Mean Field Game of Mutual Cross-Holding

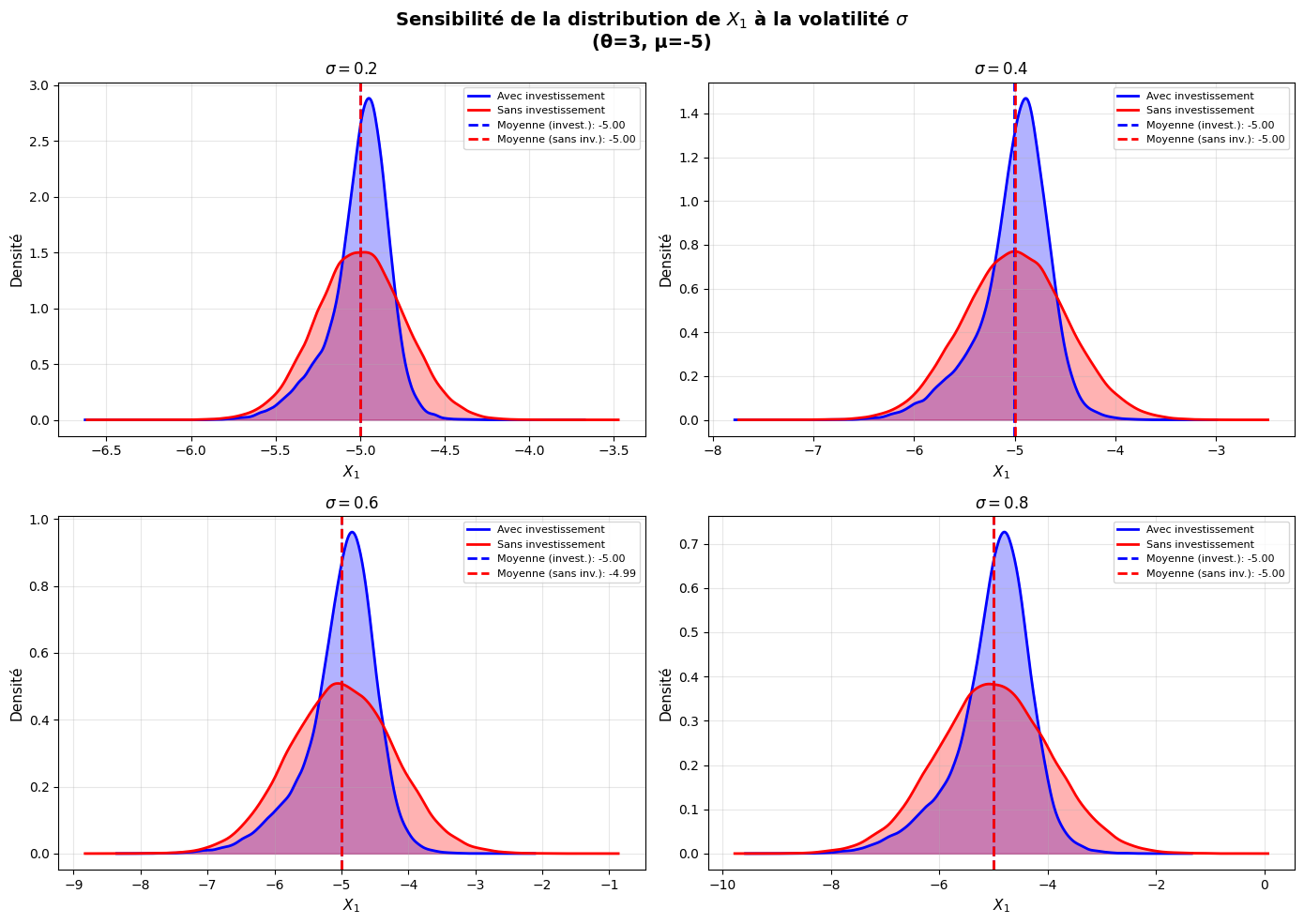

Modeled a mutual holding situation through mean field games in discrete time. Analyzed how diversification affects the total system — results consistent with the literature: optimal diversification reduces shareholders' risk.